Scrambling for High Ground in FEMA Flood Map Disputes

By

Bill Lucia

By

Bill Lucia

A complex cartographic process that affects flood insurance rates has stirred pushback in places like New York City and New Orleans.

When Vlad Ghelase began looking to buy a house in New Orleans about 15 years ago, one of his first steps was to mark the highest areas on an elevation map of the city.

“Before anything else,” Ghelase said during an interview on Monday, “my main criteria was to buy a house somewhere that was high.”

Eventually, he chose a home in Algiers Point where he has lived since. A real estate developer, Ghelase now owns six rental properties there as well.

The area is located in the West Bank neighborhood of Algiers, across the Mississippi from the French Quarter, at one of the bends the river makes as it snakes toward the Gulf of Mexico.

High ground is a relative term in New Orleans.

Depending on where you’re standing in Algiers Point the elevation could be between 5 and 10 feet. Maybe higher in some places, but not by much. By comparison, there are spots elsewhere in town where you could find yourself 8 feet below sea level.

When Hurricane Katrina struck New Orleans in 2005, the streets of Algiers Point remained unflooded.

“It’s high, it’s never gonna flood,” Ghelase said.

“If it does, even from a levee breach, the water will very quickly dissipate because everything else around us on the West Bank, towards Jefferson Parish and Harvey, and all those areas, it’s 7 to 8 feet lower,” he added. “That’s where the water’s going to go.”

An Unwelcome Update

But the Federal Emergency Management Agency—at least for now—has taken a less optimistic view than the one expressed by Ghelase about the flooding hazards in Algiers Point.

In a set of preliminary flood insurance rate maps the agency issued for New Orleans last year, parts of Algiers Point are included in what’s known as the “100-year floodplain,” a designation that means an area has at least a 1 percent annual chance of flooding. Last revised in 1984, the current map for Algiers Point classifies these parts of the neighborhood as less flood-prone.

FEMA is working toward updating the maps for areas throughout the United States. They are a key factor in determining rates under the federally administered National Flood Insurance Program. Compared to those in less-risky zones, property owners in the 100-year floodplain wind up paying higher flood insurance premiums. For most properties with mortgages in flood hazard areas this insurance is not optional, it’s a federal requirement.

The flood hazard zones also have the potential to affect local building regulations, which can create additional costs for property owners. And research has also shown that housing prices in floodplains are lower compared to those in areas considered less likely to flood.

So, with money at stake, updating the flood maps can become a bit sticky.

In an attempt to get the flood risk for Algiers Point lowered in the proposed maps, Ghelase and about 70 other neighborhood property owners filed a formal appeal with FEMA in August.

The city followed suit, filing an appeal of its own that mirrors the one the citizens submitted.

Ghelase believes the stakes of the appeal are high. If the maps are approved as currently proposed, he thinks they would stymie home sales and property renovations in Algiers Point, while also driving up rents, as landlords pass on higher insurance costs to tenants.

“It’s a mess, it’s taking all of my time,” he said of the appeal process. “But we have to do it.”

The Other Side of a Line

The situation surrounding the map for Algiers Point is not altogether unique. Appeals over preliminary flood maps have been lodged in places across the U.S., from communities at the mouth of the Columbia River in Oregon, to Palm Beach County in Florida.

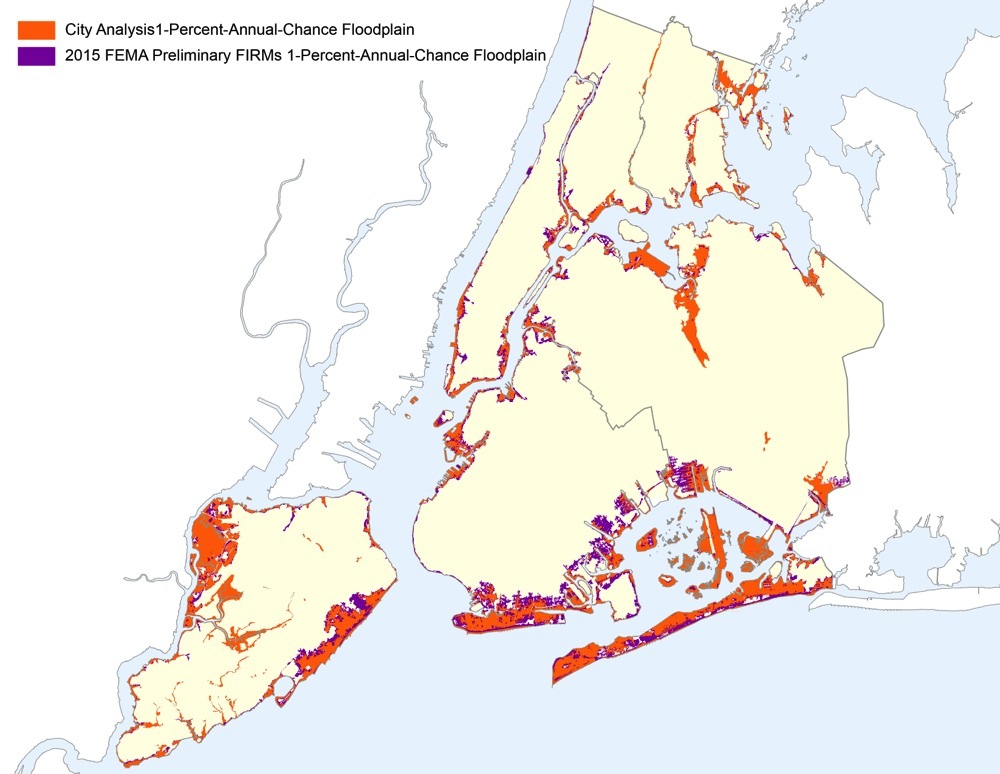

New York City has mounted one of the higher profile challenges, arguing that FEMA should remove about 26,500 properties from the 100-year floodplain in a set of preliminary maps issued for the Big Apple in 2013.

FEMA was unable to respond to a request for comment on this story, or to provide information about how many appeals are currently pending, or how much land nationwide has been moved in and out of flood hazard areas in the most recent round of map updates.

But Chad Berginnis, executive director of the Association of State Floodplain Managers, said that it has been his understanding that, compared to the overall number of flood maps FEMA issues annually, the proportion that get appealed is typically small.

While he acknowledged that FEMA has published maps in the past that have contained errors, Berginnis also said that “by and large they’re producing pretty good products.”

“What people tend to be arguing is a matter of precision they want to see in a flood map in their particular area, because they want to be on the other side of a line, so they don’t have to buy flood insurance,” he said. “That, ultimately, is what 95 percent of these appeals are about.”

When people look at the maps and consider only insurance costs, Berginnis said that it can have unwelcome consequences from a floodplain manager’s perspective.

“Often, people think their flood risk ends at some kind of delineation line and, in fact, it absolutely doesn’t,” he said.

“Mother Nature doesn’t respect the term 100-year flood,” Berginnis added. “If you get a 101-year flood, you’re screwed.”

‘We’re Concerned About Affordability’

New York filed its appeal on June 26, saying that a consulting firm it hired found errors with the methodology behind FEMA’s preliminary flood maps for the city.

“The floodplain is indeed growing, but just not nearly as much as FEMA is indicating,” Daniel Zarrilli, director of the New York City Mayor's Office of Recovery and Resiliency, said during an interview on Monday.

A substantial amount of complex science and engineering goes into producing the maps. But in a nutshell, the inaccuracies the city claims to have identified hinge on two main areas. One has to do with storm modeling, the other has to do with tidal effects.

According to figures the Mayor’s Office provided, the preliminary flood maps include 71,500 buildings in the 100-year floodplain. Based on the city’s analysis, this number should be 45,000.

“We’re concerned about affordability, and making sure that we are able to think about how our neighborhoods are going to react to drastic changes in the floodplain and the flood insurance rates,” Zarrilli said. He pointed out that the city recommends that property owners in areas considered to be less flood-prone still buy flood insurance.

“It just may be more affordable,” he said, “if they find themselves outside of the delineated 100-year floodplain.”

Berginnis, of the Association of State Floodplain Managers, suggested that the number of additional property owners that would need to buy flood insurance based on the preliminary maps for New York, could have created political pressure for the city to file its appeal.

Alluding to Hurricane Sandy, which slammed the city in 2012, he said: “This isn’t FEMA’s first rodeo mapping areas after a disaster.” When Sandy hit New York, it caused extensive flooding, widespread power outages and 43 deaths. Berginnis believes FEMA would have drawn the maps anticipating scrutiny from lawmakers, residents and the media.

“You can’t really get more of a highly watched mapping process,” he said. “I will be shocked if there’s a finding that FEMA’s mapping data is wrong.”

Since Sandy, New York has directed millions of dollars toward projects designed to protect the city against extreme weather. Just last week, Mayor Bill de Blasio announced that $100 million would be spent on flood-prevention measures for lower Manhattan.

Zarrilli highlighted these sorts of investments as proof of the city’s commitment to becoming more resilient to severe weather and climate change. He also noted that getting the flood maps right is important for guiding New York’s work in this area.

“We’re trying to get an accurate assessment,” he said. “Because so much of our planning efforts for climate change are based on what FEMA is indicating the floodplain risk to be.”

‘They’ve Been Waiting for This New Map’

Looking beyond the appeals, there are also places where people are eager for new maps to be adopted.

During the last decade, Sioux Falls, South Dakota, has made about $65 million of levee upgrades, which should reduce the number of properties within the city’s floodplain.

Two waterways slice through the west side of the city, the Big Sioux River, and Skunk Creek.

According to Jeff Schmitt, the chief planning and zoning official for the city, most of the major floods come from the Big Sioux and are triggered by snowmelt or rainfall.

Floods from heavy rain swept through the south end of Sioux Falls late last week. But Schmitt noted: “It wasn’t really a river or a creek flood, it was just more street flow.”

Built in the 1960s, the levee system was not taken into account in 2009 flood insurance rate maps for Sioux Falls. FEMA had told the city the system needed upgrades. In those 2009 maps, 2,400 properties fall within in the city’s designated floodplain, according to Schmitt.

With the levee work finished, and factored into the new maps that are expected to be finalized next year, the number of properties in the floodplain should drop to around 500, he said.

The area on the west side of the city that the mapping changes will affect, is a mix of commercial and residential buildings. City regulations can make commercial construction in the floodplain cost prohibitive, Schmitt said. And some developers have held off on projects in the area. When the floodplain boundaries change, Schmitt estimated that between eight and 10 property owners would likely move forward with projects in the $5 million to $10 million range.

“They’ve been waiting for this new map to go into effect,” he said, “so they can build where they want to.”

‘Not Going to Sit Quietly’

As it stands in New Orleans, the effects of the preliminary flood maps are looking to be less dramatic outside of Algiers Point.

According to the Mayor’s Office, 44.4 percent of the city’s population would see no change in the classification of the flood zone where they’re living, while 52.9 percent would see an improvement, under the preliminary flood insurance rate maps FEMA has issued.

Jared Munster is director of the New Orleans Department of Safety and Permits. He said during an interview on Tuesday that the improvements in flood zone classifications for parts of the city could be largely attributed to work that has been carried out in recent years to beef up flood protection, including levees and drainage systems.

But Ghelase, the resident in Algiers Point, remains skeptical about how well the levees will perform if another powerful hurricane hits.

“It will flood in the same places it flooded before,” he said, referring to the city. “Geography doesn’t change.” And that’s part of what bothers him so much about the maps. “Those areas that flooded will pay less than they did before just because of the chest-thumping about what great levees we have,” Ghelase added. “On the other hand us, we do have better flood protection, we are protected by geography and topography, we’ll pay more, which is unfair”

Ghelase said he carries flood insurance on his properties now because he’s “paranoid.” The policy for his own home runs about $460 annually. The cost is around $620 for his rentals.

“If I get hit with, say a $3,000 increase, I need to pass it to my tenants,” he said. “That’s probably not manageable.”

One of the issues at the heart of the Algiers Point appeal is whether trees lining Opelousas Avenue were mistaken for a ridge in satellite imagery, throwing off the elevation in the proposed flood map. Another is whether the FEMA analysis accounted for changes to drainage culverts in the area, which should increase the amount of water flowing away from the city during a storm.

Munster said that FEMA has acknowledged unofficially that the ridge along Opelousas was likely a mistake. The city has until Sept. 21, he said, to submit further data about the culverts. City engineers and the public works department are assisting with that effort.

“I am fully confident that we are correct in our appeal,” Munster added. He also noted that the city’s appeal extends beyond just Algiers Point, to parts of the surrounding Algiers neighborhood.

But despite his confidence, Munster is not certain that FEMA will end up changing the maps. “They may say ‘you actually are correct, there’s not a ridge here, however we don’t believe it’s going to make a difference, therefore we’re not going to run new models.’” he explained. “That we have no control over.”

Ghelase said he and the other residents involved in the appeal would continue to fight the maps as long as Algiers Point is included in a flood zone. “This affects the whole neighborhood,” he said. “They’re not going to sit quietly.”

Bill Lucia is a Reporter for Government Executive’s Route Fifty.

NEXT STORY: Fort Worth Is Sharing Data With the Private Sector Faster